The Hormuz Energy Shock and the Rate Cycle That Won't End

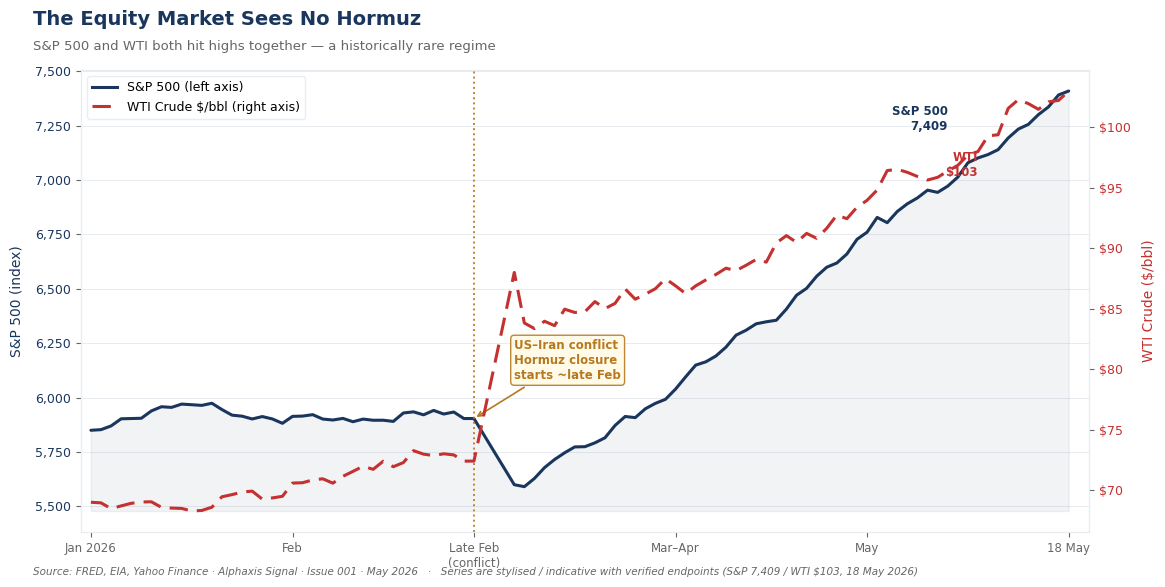

The critical distinction from every prior energy shock is the rate environment into which this one landed. In 1973, 1990, and 2022, oil spiked as equities fell — the classic stagflationary sequence. Here, the S&P 500 is at record territory while WTI sits at $103: the market is betting the Fed stays patient, the energy shock is temporary, and growth does not break. That is the bet Figure 1 puts in plain sight. UK 10-year gilts at 5.19% (Trading Economics, 18 May 2026) — a level last seen July 2008 — and a Fed hike probability at ~30% by December 2026 (CME FedWatch proxy) suggest the bond market is less sanguine.

Partial ceasefire or conflict de-escalation restores some Hormuz traffic over the 3–6 month horizon, crude prices retreat meaningfully from current levels, energy CPI begins its lagged descent through Q3, and the Fed holds rates through year-end without hiking. Long yields stabilise or ease modestly. The market relief rally on ceasefire news would be sharp but potentially short-lived if the underlying fiscal position has deteriorated — two false starts have already proved this pattern.

Inflation-linked bond markets: The 10-year TIPS breakeven (indicative ~2.5%) is not obviously mis-priced in the base case. But in the adverse scenario, breakevens re-rate materially — inflation-linked debt may outperform nominal duration if energy costs continue embedding in production chains and inflation expectations drift higher. The direction of the breakeven rate relative to current levels is the signal to watch.

WTI forward curve monitoring for backwardation persistence: The current WTI forward curve is in backwardation — front-month contracts priced above longer-dated ones — the classic supply-shock structure. What matters for the medium-term view is whether the 12-month forward price holds firm even as spot softens on ceasefire news; a persistent backwardation structure would signal the market believes the supply story is structural, not temporary.

Defensive equity sector rotation: The rate environment — 10-year at 4.63%, hike probability non-trivial — compresses multiples on growth equities and creates a relative bid for cash-generative, low-duration sectors: energy producers, utilities (where regulatory pass-through is intact), healthcare, and consumer staples. The Friday 15 May sell-off (S&P −1.2%, Nasdaq −1.5%) began to show this rotation signature. If this rotation broadens in June, it is a regime signal.

Gold dynamics: Gold at ~$4,545/oz (Trading Economics, 18 May 2026) carries significant excess over what the real-yield model would imply — that excess represents geopolitical fear premium. If the Hormuz situation deteriorates further, this premium may expand. Conversely, a swift and credible resolution to the conflict could see the geopolitical component of the gold price unwind.

- WTI crude: Watch whether spot prices soften materially on any ceasefire news — a sustained retreat from current levels would signal the market is pricing real resolution rather than a temporary pause.

- US 10-year yield: The direction of the yield relative to current levels (4.63%) is the regime indicator. A sustained move higher would shift market pricing toward the hike scenario; a sustained retreat would signal normalisation is being priced.

- Gold: Watch for gold either extending above current levels (geopolitical escalation signal) or retreating meaningfully from current levels (normalisation signal).

- DXY: A strengthening dollar relative to current levels, particularly against EM currencies, would be consistent with the adverse scenario playing out.

The primary risk is a rapid, durable ceasefire that reopens Hormuz to normal transit within 30 days. Historical oil-shock precedents (Gulf War 1991, Libya 2011) suggest supply disruptions of this scale typically resolve faster than the market prices at peak fear. If resolution occurs in June and WTI retraces toward $80, energy CPI begins falling with the typical 3-month lag, and the entire higher-for-longer repricing unwinds — bonds rally, growth sectors recover sharply. The second risk is OPEC+ response: Saudi Arabia and the UAE have spare capacity (indicative 2–3 million bpd, per IEA estimates) and could partially offset Hormuz losses if incentivised to do so, potentially taking $15–20 off the front-month WTI price.